Home » Rishi Sunak

Category Archives: Rishi Sunak

Virus Economics: When Markets Feel Poorly

Fearing that the Coronavirus pandemic might affect their investments, perception became reality for investors in the world’s stock exchanges as markets see their biggest drop in recent years.

‘Money flees uncertainty’ – You’ve heard it before or read it in print

It vaporizes during civil unrest, it dissipates into thin air when politics goes awry such as when a national leader faces a coup d’é·tat, and it leaves without saying goodbye during natural disasters. In short, the thing we call “money” isn’t our friend at all, in fact, “money” (by which, I mean ‘investment’) is the most fair-weather friend we could have.

And that’s a good thing!

(I hear what you’re thinking, “Is Gordon Gekko writing this post? You know, the whole, “Greed is good,” thing and all that?) Hehehe.

No, Gordon Gekko from the movie Wall Street isn’t writing this post, I’m merely remarking upon what’s patently obvious in the global marketplace — that the de facto rule is that individual and institutional investors prefer stable and profitable companies and countries to unstable and less profitable companies and countries. Of course.

What it means on the ground is that organizations that prepare in advance for the ‘bad times’ are seen as more stable, and therefore a better long-term investment, and that’s where the money flees to during challenging economic times.

Which is why some countries have a AAA+ credit rating and others don’t. It’s why some companies have triple A credit and others don’t. It’s why some countries need IMF loans and others don’t.

Stayin’ Alive, Yeah!

Being prepared, means staying alive, even while your competitors are dying all around you. (Not literally dying; But that’s the kind of talk you hear on trading floors during the so-called ‘bad times’)

I say ‘bad times’ because, for prepared countries (and companies) there really are no ‘bad times’.

Prepared organizations sail right through recessions, depressions, war, civil unrest, natural disasters and more — precisely because they’re well managed and well-equipped to weather any sort of storm, whether it be political, economic, or even natural disasters that can strike without warning.

Any CFO knows that recessions occur every 25-years. They know their factory (or whatever) is located in a floodplain, or in an active earthquake zone, etc., therefore, long in advance of any of those events occurring, they create a ‘rainy day fund’ to carry the company through a catastrophic period with surprisingly little upset.

The reward for this kind of long-term thinking is that when disaster finally strikes (and it surely will, it’s just a question of when) your organization will carry-on with ‘business as usual’ even as your competitors are dying in the market. It’s called ‘building resiliency’ into your company (or country) and it’s a fine thing.

And that’s the time that your company can go ’round and snap those companies up for ten cents on the dollar. ‘Picking their bones’ as we used to say in the halcyon days of Carl Icahn, investor, corporate raider… and strangely enough… philanthropist. Cool, huh?

Anyway, ‘Fortune favours the prepared’ said Louis Pasteur, and he was right.

So it follows then, that countries that aren’t prepared for Coronavirus version 2019 (called COVID-19 now that it’s been officially named) aren’t going to sail through it unaffected.

Rather, it’s easy to see even at this early stage which countries have engaged in long-term thinking, and have long ago upgraded their medical capacities to handle pandemics such as COVID-19, and although some cases showed up on their healthcare systems they had the ability and the capacity to deal with those cases with immediacy.

And if there’s one thing that pandemic-type viruses hate, it’s timely diagnosis, speedy quarantine and effective treatment.

Consequently, those prepared economies will see little economic impact from COVID-19 or any subsequent mutation of the COVID-19 virus which is likely to be called COVID-20 if it occurs in 2020. And there’s always, always, a mutation eventually, however it’s almost impossible to predict when that mutation will occur. At that time, the treatment for COVID-19 won’t work on COVID-20 (or whatever that mutation gets named) or if it does work, it’s likely to be less than 50% effective. Just sayin’.

Again, those governments that believe in long-term thinking and have prepared in advance of the latest Coronavirus pandemic have already inoculated their economies against the worst of the problem, although they could still (secondarily) be affected by other countries whose economies may now suffer on account of not being prepared.

Therefore, it was the perception of investors who have themselves created the entire ‘Black Monday’ market devaluation by pulling their investments from the stock market. But if there are more countries that are prepared for and respond well to the Coronavirus threat, then today’s market recalibration will turn out to be nothing more than a blip on the year-end 2020 annual report.

But if it turns out that a majority of countries aren’t properly prepared to handle this Coronavirus pandemic then this market slide could last a long time and worsen as thousands more become infected.

And then what happens around November or December 2020 if a new, mutated COVID virus appears?

Just as the markets get back to normal, suddenly a newer and more virulent version of this virus begins to run through the world’s healthcare systems… will they be ready then? Let’s hope so.

More Pandemics are On the Way. So, Let’s be Ready Next Time!

One thing’s for certain. In this increasingly interconnected world, there will be more pandemics and perhaps much more deadly and with a more rapid onset than the COVID-19 virus.

In such an instance, only the countries blessed with leaders who aren’t afraid to make the big decisions (like closing their airports and even their land borders and seaports for 2-weeks to prevent millions more infections from occurring) will survive the next viral onslaught.

In the case of the COVID-19 virus (so far) it looks like the major economies have dodged a bullet, because it turns out that it isn’t the strongest virus, as it’s only able to kill the elderly and the infirm. However, future pandemics may not be as mild as this particular Coronavirus.

We need to get ready. We have so far failed this drill, but Western healthcare systems are quickly ramping-up to meet the present threat. Until governments begin to provide permanent ongoing funding to healthcare providers to help them get more efficient at capturing such viral threats, isolating those who are contagious, and effectively treating those who’ve been exposed to such contagions, we’re living on borrowed time.

Let us thank the medical professionals on the front lines diagnosing, isolating, and treating those people who’ve had exposure to the virus, and thank them for doing much in a short time, with only tepid support (at first) from Western governments. Bravo!

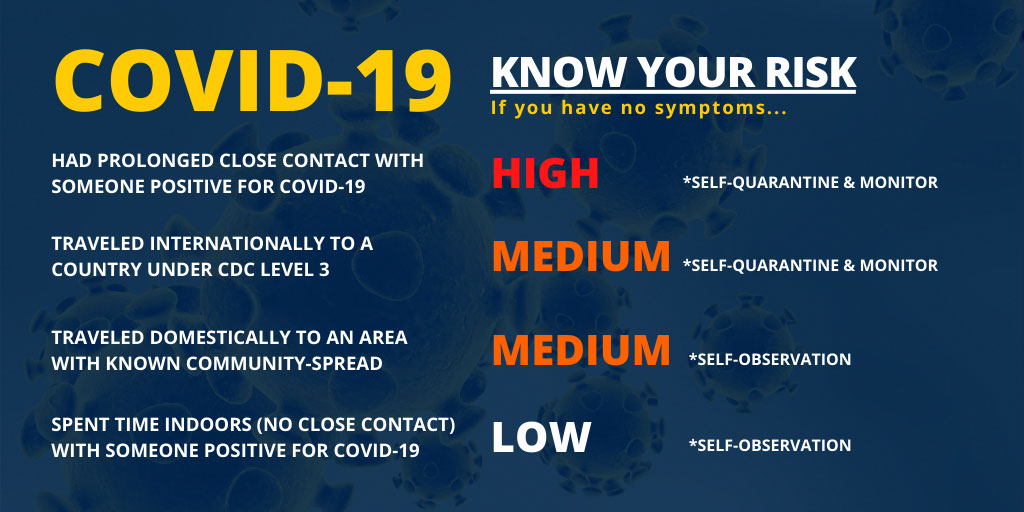

Bonus Graphic

Markets see their biggest drop in recent years as fear of the COVID-19 virus spreads.

UK Budget 2020: How to Deliver on Promises Without Breaking the Bank

Nobody likes paying taxes, that’s understood.

But sometimes, in order to fulfil the promises made during an election — the promises that were made to appease and please those who voted the present government into office! — taxation levels must accordingly increase to provide the things that voters have hired the government to accomplish.

The trick for governments is how to keep their election promises without losing the confidence of voters, and I therefore offer the following well-meant suggestions using the proven example of Canada’s economic miracle during the 1994-2015 timeframe:

- As in Canada, the national GST rate in the UK should be set to 7% and should always hover between 5% and 10% in order to arrive at a zero-deficit budget, year-in and year-out. The GST shouldn’t be required to do anything else except to balance the budget, or, in the best-case scenario, to paydown some amount of government debt during any subsequent economic ‘boom years’ for the economy. That keeps it simple. (Although Canada has strayed from this plan recently and is now beginning to pay a price for its lack of committent to it’s formerly strict budgetary goals).

- The national GST should apply to every single transaction in the UK and only medical items should be exempt, such as female hygiene products, emergency medical kits, plasters/band-aids, prescription medications, and diagnostic imaging equipment like MRI’s and Cat Scan’s etc.

- Other than those exceptions, not one thing should be exempt from the national GST which would raise the total tax take for the government by a significant amount. (This plan worked wonders for Canada when it was in an economic tailspin) See: Jean Chretien: Lessons from Canada’s ‘basket case’ moment.

- Things like fuel (any kind of fuel, such as fuel for aircraft, cars, pleasure boats and ships, locomotives, home heating fuels like kerosene or natural gas, coal, firewood, wood pellets, etc.) and every other thing that is sold in the UK should be GST taxable, including financial transactions of any kind, including fees paid for legal or financial advice, and on the fees to purchase mutual funds, bonds, and other financial instruments, and on homes, cars, lumber, kitchen gadgets, and every item or service sold in the UK.

- Also, part of Canada’s economic miracle which began in the 1990’s was to lower corporate tax rates to 15%, then 14.5% and finally to 14% over a number of years, with a special tax rate of 10% for small-cap companies. This stimulated SME growth in the country that continues to this day, Indeed, Canada barely noticed the global financial crisis of 2007-2009, and it remained the fastest growing G7 economy before, during, and for a time after the U.S. subprime mortgage crisis.

- The other important part of Canada’s economic miracle of the 1990’s and early 2000’s is that the government got rid of wasteful and overlapping government programmes — basically telling every government department that they had 5% “fat” built-in to their annual budgets and that each department (except for the Department of Defence) would be required to submit budget proposals for the next 3-years showing a 5% spending cut from planned spending levels — or the government would simply lop 5% ‘right off the top’ from said department without any further warning or consultation.

- Not only did these things work well, but Canada also managed to make significant payments to paydown the government debt which was negatively affecting the economy and was costing a fortune in annual debt servicing costs. This in turn, allowed the Canadian government more room to manoeuvre from a federal budget perspective in subsequent years as less government revenue was required to service the accumulated deficits (debt) of Canada’s federal government.

- The next government that came into power after Liberal Party of Canada’s Jean Chretien and Paul Martin, was Stephen Harper’s Conservative government which in 2015 implemented a brilliant stimulus package (a home renovation tax credit) that boosted the Canadian economy with only a tiny amount of stimulus. Which, as it happened, put every available tradesperson in the country to work for a full 3-years just to meet the demand. So many Canadians decided to spend more than the allowable $5000. tax credit amount to renovate their homes… that home building centres, home decorating centres, and car dealerships that sell tradesman vans and trucks could barely keep up with demand. It was the perfect solution to boost the economy after years of budget cuts designed to balance the federal government budget.

This image is familiar to Canadian taxpayers as it appears frequently on income tax related documents, showing where each taxation dollar is spent by the federal government of Canada. Image courtesy of Canada Revenue Agency

Rather than trying to reinvent the wheel, the new Chancellor of the Exchequer, Rishi Sunak might consider following the tried-and-true Canadian example of ending the many complicated and difficult to administer taxes throughout the UK economy and roll them into a simplified GST with a 7% rate that taxes everything except medical supplies and equipment, followed by a plan to lower government deficits to zero over 5-years (with legally-enforceable punishments for the government if it fails to meet its zero deficit targets) and by lowering the corporate tax rate to match Canada’s corporate taxation rates to stimulate the economy over the medium term, and by stimulating the economy with a modest tax credit for home renovations where better home insulation is a part of that programme which works for homeowners to lower their electricity bills and further stimulate the economy over the short term.

In this way, the UK government can begin its Brexit year on a sound financial footing, losing some confusing and overlapping smallish taxes while dramatically increasing its total taxation revenue, while at the same time it attracts new businesses to the UK and supports existing UK businesses with lower corporate tax levels, and by employing every single tradesperson in the country for at least the next 3-years.

Congratulations and best wishes to the new and highly-esteemed Chancellor of the Exchequer, Mr. Rishi Sunak!